Saturday, December 22, 2012

Noahpinion: Did risky mortgage lending cause the financial cri...

Noahpinion: Did risky mortgage lending cause the financial cri...: No. Or, at least, not by itself, it did not. The financial crisis consisted of two things: 1. A liquidity crunch or bank run , in ...

Noahpinion: Macro, what have you done for me lately?

Noahpinion: Macro, what have you done for me lately?: Paul Krugman says the state of macroeconomics is rotten . Steve Williamson disagrees. With apologies, I'll cut-and-paste most of Steve's...

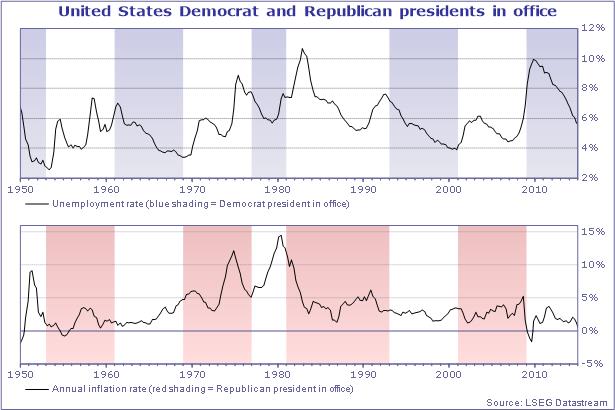

Tuesday, October 30, 2012

From Datastream:

This week’s two-pronged Chart of the Week may offer more food for debate and thought than it does clear answers. Given the number of variables that affect the U.S. economy, and the fact that today’s economy is a vastly different animal than that of the 1970s, 1980s or even 1990s (given the changes wrought by technology and globalization), the data may prove an interesting jumping off point for prognosticators interested in discussing what happens next, especially in light of the U.S. jobs market report for October, scheduled for release at the end of this week. It may end up proving to be the case, as Reuters BreakingViews suggested in this analysis, that these data points shape the election’s outcome, rather than any views of the lessons of history.

This week’s two-pronged Chart of the Week may offer more food for debate and thought than it does clear answers. Given the number of variables that affect the U.S. economy, and the fact that today’s economy is a vastly different animal than that of the 1970s, 1980s or even 1990s (given the changes wrought by technology and globalization), the data may prove an interesting jumping off point for prognosticators interested in discussing what happens next, especially in light of the U.S. jobs market report for October, scheduled for release at the end of this week. It may end up proving to be the case, as Reuters BreakingViews suggested in this analysis, that these data points shape the election’s outcome, rather than any views of the lessons of history.

Saturday, October 27, 2012

Technical Analysis

In a recent paper, Pierre Bajgrowicz and Olivier Scaillet question the profitability of technical analysis based trading strategies. I think it's an amazing paper.

Friday, October 26, 2012

Monday, October 22, 2012

Financial Crises and Recoveries

In a recent opinion column, Michael Bordo explains that financial crises in the U.S. have not necessarily been followed by weak recoveries. I like the evidence they present.

http://online.wsj.com/article/SB10000872396390444506004577613122591922992.html

http://online.wsj.com/article/SB10000872396390444506004577613122591922992.html

Michael Bordo: Financial Recessions Don't Lead to Weak Recoveries

The evidence since 1880 shows a faster pace of recovery. The Obama years are the exception.

Follow the discussion at: http://gregmankiw.blogspot.com/2012/10/john-taylor-versus-paul-krugman.html

On writing

"Any one who wishes to

become a good writer should endeavour, before he allows himself to be

tempted by the more showy qualities, to be direct, simple, brief,

vigorous, and lucid."

H.W. Fowler

Monday, October 15, 2012

Nobel Prize in Economics 2012

Well, the day finally came. Scroll down to Advanced Information and read about the work of the new Nobel Laureates at http://www.nobelprize.org/nobel_prizes/economics/laureates/2012/advanced.html

To read from Alvin Roth, visit his blog at: http://marketdesigner.blogspot.com

Here is a primer on matching theory: http://marginalrevolution.com/marginalrevolution/2012/10/noble-matching.html

To read from Alvin Roth, visit his blog at: http://marketdesigner.blogspot.com

Here is a primer on matching theory: http://marginalrevolution.com/marginalrevolution/2012/10/noble-matching.html

Thursday, March 1, 2012

Rethinking Economics in a Changed World

Joseph Stiglitz, Michael Spence, and Robert Solow talk about lessons from the U.S. Financial Crisis.

Click here>>>

Click here>>>

Economic Models: Simulations of Reality

This is a useful and easy to follow description of Economic Models.

Click here: Economic Models Explained

After reading it, you may want to take a look at this now classic piece by Krugman:

THE ACCIDENTAL THEORIST SYNOPSIS: Describes how producitivity gains are the source of all Economic good, not evil, in the world.

Imagine an economy that produces only two things: hot dogs and buns. Consumers in this economy insist that every hot dog come with a bun, and vice versa. And labor is the only input to production.

OK, timeout. Before we go any further, I need to ask what you think of an essay that begins this way. Does it sound silly to you? Were you about to turn the virtual page, figuring that this couldn't be about anything important?

One of the points of this column is to illustrate a paradox: You can't do serious economics unless you are willing to be playful. Economic theory is not a collection of dictums laid down by pompous authority figures. Mainly, it is a menagerie of thought experiments--parables, if you like--that are intended to capture the logic of economic processes in a simplified way. In the end, of course, ideas must be tested against the facts. But even to know what facts are relevant, you must play with those ideas in hypothetical settings. And I use the word "play" advisedly: Innovative thinkers, in economics and other disciplines, often have a pronounced whimsical streak.

It so happens that I am about to use my hot-dog-and-bun example to talk about technology, jobs, and the future of capitalism. Readers who feel that big subjects can only be properly addressed in big books--which present big ideas, using big words--will find my intellectual style offensive. Such people imagine that when they write or quote such books, they are being profound. But more often than not, they're being profoundly foolish. And the best way to avoid such foolishness is to play around with a thought experiment or two.

So let's continue. Suppose that our economy initially employs 120 million workers, which corresponds more or less to full employment. It takes two person-days to produce either a hot dog or a bun. (Hey, realism is not the point here.) Assuming that the economy produces what consumers want, it must be producing 30 million hot dogs and 30 million buns each day; 60 million workers will be employed in each sector.

Now, suppose that improved technology allows a worker to produce a hot dog in one day rather than two. And suppose that the economy makes use of this increased productivity to increase consumption to 40 million hot dogs with buns a day. This requires some reallocation of labor, with only 40 million workers now producing hot dogs, 80 million producing buns.

When a famous journalist arrives on the scene. He takes a look at recent history and declares that something terrible has happened: Twenty million hot-dog jobs have been destroyed. When he looks deeper into the matter, he discovers that the output of hot dogs has actually risen 33 percent, yet employment has declined 33 percent. He begins a two-year research project, touring the globe as he talks with executives, government officials, and labor leaders. The picture becomes increasingly clear to him: Supply is growing at a breakneck pace, and there just isn't enough consumer demand to go around. True, jobs are still being created in the bun sector; but soon enough the technological revolution will destroy those jobs too. Global capitalism, in short, is hurtling toward crisis. He writes up his alarming conclusions in a 473-page book; full of startling facts about the changes underway in technology and the global market; larded with phrases in Japanese, German, Chinese, and even Malay; and punctuated with occasional barbed remarks about the blinkered vision of conventional economists. The book is widely acclaimed for its erudition and sophistication, and its author becomes a lion of the talk-show circuit.

Meanwhile, economists are a bit bemused, because they can't quite understand his point. Yes, technological change has led to a shift in the industrial structure of employment. But there has been no net job loss; and there is no reason to expect such a loss in the future. After all, suppose that productivity were to double in buns as well as hot dogs. Why couldn't the economy simply take advantage of that higher productivity to raise consumption to 60 million hot dogs with buns, employing 60 million workers in each sector?

Or, to put it a different way: Productivity growth in one sector can very easily reduce employment in that sector. But to suppose that productivity growth reduces employment in the economy as a whole is a very different matter. In our hypothetical economy it is--or should be--obvious that reducing the number of workers it takes to make a hot dog reduces the number of jobs in the hot-dog sector but creates an equal number in the bun sector, and vice versa. Of course, you would never learn that from talking to hot-dog producers, no matter how many countries you visit; you might not even learn it from talking to bun manufacturers. It is an insight that you can gain only by playing with hypothetical economies--by engaging in thought experiments.

At this point, I imagine that readers have three objections. First, isn't my thought experiment too simple to tell us anything about the real world?

No, not at all. For one thing, if for "hot dogs" you substitute "manufactures" and for "buns" you substitute "services," my story actually looks quite a lot like the history of the U.S. economy over the past generation. Between 1970 and the present, the economy's output of manufactures roughly doubled; but, because of increases in productivity, employment actually declined slightly. The production of services also roughly doubled--but there was little productivity improvement, and employment grew by 90 percent. Overall, the U.S. economy added more than 45 million jobs. So in the real economy, as in the parable, productivity growth in one sector seems to have led to job gains in the other.

But there is a deeper point: A simple story is not the same as a simplistic one. Even our little parable reveals possibilities that no amount of investigative reporting could uncover. It suggests, in particular, that what might seem to a naive commentator like a natural conclusion--if productivity growth in the steel industry reduces the number of jobs for steelworkers, then productivity growth in the economy as a whole reduces employment in the economy as a whole--may well involve a crucial fallacy of composition.

But wait--what entitles me to assume that consumer demand will rise enough to absorb all the additional production? One good answer is: Why not? If production were to double, and all that production were to be sold, then total income would double too; so why wouldn't consumption double? That is, why should there be a shortfall in consumption merely because the economy produces more?

Here again, however, there is a deeper answer. It is possible for economies to suffer from an overall inadequacy of demand--recessions do happen. However, such slumps are essentially monetary--they come about because people try in the aggregate to hold more cash than there actually is in circulation. (That insight is the essence of Keynesian economics.) And they can usually be cured by issuing more money--full stop, end of story. An overall excess of production capacity (compared to what?) has nothing at all to do with it.

Perhaps the biggest objection to my hot-dog parable is that final bit about the famous journalist. Surely, no respected figure would write a whole book on the world economy based on such a transparent fallacy. And even if he did, nobody would take him seriously.

But while the hot-dog-and-bun economy is hypothetical, the journalist is not. Rolling Stone reporter William B. Greider has just published a widely heralded new book titled One World, Ready or Not: The Manic Logic of Global Capitalism. And his book is exactly as I have described it: a massive, panoramic description of the world economy, which piles fact upon fact (some of the crucial facts turn out to be wrong, but that is another issue) in apparent demonstration of the thesis that global supply is outrunning global demand. Alas, all the facts are irrelevant to that thesis; for they amount to no more than the demonstration that there are many industries in which growing productivity and the entry of new producers has led to a loss of traditional jobs--that is, that hot-dog production is up, but hot-dog employment is down. Nobody, it seems, warned Greider that he needed to worry about fallacies of composition, that the logic of the economy as a whole is not the same as the logic of a single market.

I think I know what Greider would answer: that while I am talking mere theory, his argument is based on the evidence. The fact, however, is that the U.S. economy has added 45 million jobs over the past 25 years--far more jobs have been added in the service sector than have been lost in manufacturing. Greider's view, if I understand it, is that this is just a reprieve--that any day now, the whole economy will start looking like the steel industry. But this is a purely theoretical prediction. And Greider's theorizing is all the more speculative and simplistic because he is an accidental theorist, a theorist despite himself--because he and his unwary readers imagine that his conclusions simply emerge from the facts, unaware that they are driven by implicit assumptions that could not survive the light of day.

Needless to say, I have little hope that the general public, or even most intellectuals, will realize what a thoroughly silly book Greider has written. After all, it looks anything but silly--it seems knowledgeable and encyclopedic, and is written in a tone of high seriousness. It strains credibility to assert the truth, which is that the main lesson one really learns from those 473 pages is how easy it is for an intelligent, earnest man to trip over his own intellectual shoelaces.

Why did it happen? Part of the answer is that Greider systematically cut himself off from the kind of advice and criticism that could have saved him from himself. His acknowledgements conspicuously do not include any competent economists--not a surprising thing, one supposes, for a man who describes economics as "not really a science so much as a value-laden form of prophecy." But I also suspect that Greider is the victim of his own earnestness. He clearly takes his subject (and himself) too seriously to play intellectual games. To test-drive an idea with seemingly trivial thought experiments, with hypothetical stories about simplified economies producing hot dogs and buns, would be beneath his dignity. And it is precisely because he is so serious that his ideas are so foolish.

Click here: Economic Models Explained

After reading it, you may want to take a look at this now classic piece by Krugman:

Imagine an economy that produces only two things: hot dogs and buns. Consumers in this economy insist that every hot dog come with a bun, and vice versa. And labor is the only input to production.

OK, timeout. Before we go any further, I need to ask what you think of an essay that begins this way. Does it sound silly to you? Were you about to turn the virtual page, figuring that this couldn't be about anything important?

One of the points of this column is to illustrate a paradox: You can't do serious economics unless you are willing to be playful. Economic theory is not a collection of dictums laid down by pompous authority figures. Mainly, it is a menagerie of thought experiments--parables, if you like--that are intended to capture the logic of economic processes in a simplified way. In the end, of course, ideas must be tested against the facts. But even to know what facts are relevant, you must play with those ideas in hypothetical settings. And I use the word "play" advisedly: Innovative thinkers, in economics and other disciplines, often have a pronounced whimsical streak.

It so happens that I am about to use my hot-dog-and-bun example to talk about technology, jobs, and the future of capitalism. Readers who feel that big subjects can only be properly addressed in big books--which present big ideas, using big words--will find my intellectual style offensive. Such people imagine that when they write or quote such books, they are being profound. But more often than not, they're being profoundly foolish. And the best way to avoid such foolishness is to play around with a thought experiment or two.

So let's continue. Suppose that our economy initially employs 120 million workers, which corresponds more or less to full employment. It takes two person-days to produce either a hot dog or a bun. (Hey, realism is not the point here.) Assuming that the economy produces what consumers want, it must be producing 30 million hot dogs and 30 million buns each day; 60 million workers will be employed in each sector.

Now, suppose that improved technology allows a worker to produce a hot dog in one day rather than two. And suppose that the economy makes use of this increased productivity to increase consumption to 40 million hot dogs with buns a day. This requires some reallocation of labor, with only 40 million workers now producing hot dogs, 80 million producing buns.

When a famous journalist arrives on the scene. He takes a look at recent history and declares that something terrible has happened: Twenty million hot-dog jobs have been destroyed. When he looks deeper into the matter, he discovers that the output of hot dogs has actually risen 33 percent, yet employment has declined 33 percent. He begins a two-year research project, touring the globe as he talks with executives, government officials, and labor leaders. The picture becomes increasingly clear to him: Supply is growing at a breakneck pace, and there just isn't enough consumer demand to go around. True, jobs are still being created in the bun sector; but soon enough the technological revolution will destroy those jobs too. Global capitalism, in short, is hurtling toward crisis. He writes up his alarming conclusions in a 473-page book; full of startling facts about the changes underway in technology and the global market; larded with phrases in Japanese, German, Chinese, and even Malay; and punctuated with occasional barbed remarks about the blinkered vision of conventional economists. The book is widely acclaimed for its erudition and sophistication, and its author becomes a lion of the talk-show circuit.

Meanwhile, economists are a bit bemused, because they can't quite understand his point. Yes, technological change has led to a shift in the industrial structure of employment. But there has been no net job loss; and there is no reason to expect such a loss in the future. After all, suppose that productivity were to double in buns as well as hot dogs. Why couldn't the economy simply take advantage of that higher productivity to raise consumption to 60 million hot dogs with buns, employing 60 million workers in each sector?

Or, to put it a different way: Productivity growth in one sector can very easily reduce employment in that sector. But to suppose that productivity growth reduces employment in the economy as a whole is a very different matter. In our hypothetical economy it is--or should be--obvious that reducing the number of workers it takes to make a hot dog reduces the number of jobs in the hot-dog sector but creates an equal number in the bun sector, and vice versa. Of course, you would never learn that from talking to hot-dog producers, no matter how many countries you visit; you might not even learn it from talking to bun manufacturers. It is an insight that you can gain only by playing with hypothetical economies--by engaging in thought experiments.

At this point, I imagine that readers have three objections. First, isn't my thought experiment too simple to tell us anything about the real world?

No, not at all. For one thing, if for "hot dogs" you substitute "manufactures" and for "buns" you substitute "services," my story actually looks quite a lot like the history of the U.S. economy over the past generation. Between 1970 and the present, the economy's output of manufactures roughly doubled; but, because of increases in productivity, employment actually declined slightly. The production of services also roughly doubled--but there was little productivity improvement, and employment grew by 90 percent. Overall, the U.S. economy added more than 45 million jobs. So in the real economy, as in the parable, productivity growth in one sector seems to have led to job gains in the other.

But there is a deeper point: A simple story is not the same as a simplistic one. Even our little parable reveals possibilities that no amount of investigative reporting could uncover. It suggests, in particular, that what might seem to a naive commentator like a natural conclusion--if productivity growth in the steel industry reduces the number of jobs for steelworkers, then productivity growth in the economy as a whole reduces employment in the economy as a whole--may well involve a crucial fallacy of composition.

But wait--what entitles me to assume that consumer demand will rise enough to absorb all the additional production? One good answer is: Why not? If production were to double, and all that production were to be sold, then total income would double too; so why wouldn't consumption double? That is, why should there be a shortfall in consumption merely because the economy produces more?

Here again, however, there is a deeper answer. It is possible for economies to suffer from an overall inadequacy of demand--recessions do happen. However, such slumps are essentially monetary--they come about because people try in the aggregate to hold more cash than there actually is in circulation. (That insight is the essence of Keynesian economics.) And they can usually be cured by issuing more money--full stop, end of story. An overall excess of production capacity (compared to what?) has nothing at all to do with it.

Perhaps the biggest objection to my hot-dog parable is that final bit about the famous journalist. Surely, no respected figure would write a whole book on the world economy based on such a transparent fallacy. And even if he did, nobody would take him seriously.

But while the hot-dog-and-bun economy is hypothetical, the journalist is not. Rolling Stone reporter William B. Greider has just published a widely heralded new book titled One World, Ready or Not: The Manic Logic of Global Capitalism. And his book is exactly as I have described it: a massive, panoramic description of the world economy, which piles fact upon fact (some of the crucial facts turn out to be wrong, but that is another issue) in apparent demonstration of the thesis that global supply is outrunning global demand. Alas, all the facts are irrelevant to that thesis; for they amount to no more than the demonstration that there are many industries in which growing productivity and the entry of new producers has led to a loss of traditional jobs--that is, that hot-dog production is up, but hot-dog employment is down. Nobody, it seems, warned Greider that he needed to worry about fallacies of composition, that the logic of the economy as a whole is not the same as the logic of a single market.

I think I know what Greider would answer: that while I am talking mere theory, his argument is based on the evidence. The fact, however, is that the U.S. economy has added 45 million jobs over the past 25 years--far more jobs have been added in the service sector than have been lost in manufacturing. Greider's view, if I understand it, is that this is just a reprieve--that any day now, the whole economy will start looking like the steel industry. But this is a purely theoretical prediction. And Greider's theorizing is all the more speculative and simplistic because he is an accidental theorist, a theorist despite himself--because he and his unwary readers imagine that his conclusions simply emerge from the facts, unaware that they are driven by implicit assumptions that could not survive the light of day.

Needless to say, I have little hope that the general public, or even most intellectuals, will realize what a thoroughly silly book Greider has written. After all, it looks anything but silly--it seems knowledgeable and encyclopedic, and is written in a tone of high seriousness. It strains credibility to assert the truth, which is that the main lesson one really learns from those 473 pages is how easy it is for an intelligent, earnest man to trip over his own intellectual shoelaces.

Why did it happen? Part of the answer is that Greider systematically cut himself off from the kind of advice and criticism that could have saved him from himself. His acknowledgements conspicuously do not include any competent economists--not a surprising thing, one supposes, for a man who describes economics as "not really a science so much as a value-laden form of prophecy." But I also suspect that Greider is the victim of his own earnestness. He clearly takes his subject (and himself) too seriously to play intellectual games. To test-drive an idea with seemingly trivial thought experiments, with hypothetical stories about simplified economies producing hot dogs and buns, would be beneath his dignity. And it is precisely because he is so serious that his ideas are so foolish.

The Case for a Managed Float under Inflation Targeting

Here is a nice discussion on alternative monetary policy for emerging countries.

Click Here to View Content

Click Here to View Content

Wednesday, February 8, 2012

Friday, February 3, 2012

Economic Insight

Here you can find some interesting videos form MIT. These videos present insightful views about many aspects of the world. Of particular interest to me are the one related to economic and finance.

Wednesday, January 25, 2012

Free and Open Access Books

Here is a collection of websites offering free and open access books:

Intech Open

Financial Economics Lecture Notes

Intech Open

Financial Economics Lecture Notes

Friday, January 20, 2012

Optimization Algorithms

There are many situations in which one needs reliable optimization algorithms to solve econometric and statistical problems. I use them mostly for Maximum Likelihood and Generalized Method of Moments estimations. I find the following algorithms useful, flexible, and very powerful:

NLopt:

NLopt is a free/open-source library for nonlinear optimization, providing a common interface for a number of different free optimization routines available online as well as original implementations of various other algorithms. Its features include:

NLopt:

NLopt is a free/open-source library for nonlinear optimization, providing a common interface for a number of different free optimization routines available online as well as original implementations of various other algorithms. Its features include:

- Callable from C, C++, Fortran, Matlab or GNU Octave, Python, GNU Guile, and GNU R.

- A common interface for many different algorithms—try a different algorithm just by changing one parameter.

- Support for large-scale optimization (some algorithms scalable to millions of parameters and thousands of constraints).

- Both global and local optimization algorithms.

- Algorithms using function values only (derivative-free) and also algorithms exploiting user-supplied gradients.

- Algorithms for unconstrained optimization, bound-constrained optimization, and general nonlinear inequality/equality constraints.

- Free/open-source software under the GNU LGPL (and looser licenses for some portions of NLopt).

Sunday, January 8, 2012

Macroeconomic Modelling

The following are two excellent tools for macroeconomic modelling:

Macroeconomic Models Data Base: It has more than 50 macroeconomic models that can be computed in Dynare. The project is headed by Volker Wieland, Professor of Monetary Theory and Policy at Goethe University Frankfurt.

DYNARE: "Dynare is a software platform for handling a wide class of economic models, in particular dynamic stochastic general equilibrium (DSGE) and overlapping generations (OLG) models." It is freely available but you have to run it in MATLAB, so, you need MatLab to be installed in your computer first.

Using Dynare to Solve DSGE Models: This is a short tutorial to get started using DYNARE by Eric Sims, University of Notre Dame. He also has nice documentation on estimating RBC and New Keynesian Models here. A similar tutorial can be found here.

Wouter den Haan: Resources for computation of DSGE models.

Macroeconomic Models Data Base: It has more than 50 macroeconomic models that can be computed in Dynare. The project is headed by Volker Wieland, Professor of Monetary Theory and Policy at Goethe University Frankfurt.

DYNARE: "Dynare is a software platform for handling a wide class of economic models, in particular dynamic stochastic general equilibrium (DSGE) and overlapping generations (OLG) models." It is freely available but you have to run it in MATLAB, so, you need MatLab to be installed in your computer first.

Using Dynare to Solve DSGE Models: This is a short tutorial to get started using DYNARE by Eric Sims, University of Notre Dame. He also has nice documentation on estimating RBC and New Keynesian Models here. A similar tutorial can be found here.

Wouter den Haan: Resources for computation of DSGE models.

R, Matlab, and Gauss Codes

Random collection of codes in R, Matlab, and Gauss for Econometrics and Macroeconomics:

Motohiro Yogo

Serena Ng

Perron

Frank Schorfheide

Frank Schorfheide

Econometric Theory

R in Finance

Econometrics Journal Online

Stochatic Frontier

Stochastic Volatility

Option Pricing

Andrew Patton

Martin Uribe

Judson Caskey (Stata, Matlab, Shumway Hazard Model)

Efficient Method of Moments Matlab

Raymond Kan

University of Zurich

Simone Manganelli

Journal of Financial Economics

Bayesian VAR

Wouter J. den Haan

Motohiro Yogo

Serena Ng

Perron

Frank Schorfheide

Frank Schorfheide

Econometric Theory

R in Finance

Econometrics Journal Online

Stochatic Frontier

Stochastic Volatility

Option Pricing

Andrew Patton

Martin Uribe

Judson Caskey (Stata, Matlab, Shumway Hazard Model)

Efficient Method of Moments Matlab

Raymond Kan

University of Zurich

Simone Manganelli

Journal of Financial Economics

Bayesian VAR

Wouter J. den Haan

Monday, January 2, 2012

A Collection of Article on the U.S. Financial Crisis 2007-2008

"Fire Sales in Finance and Macroeconomics" by Andrei Shleifer and Robert Vishny

On page 39:

Table 1: A Narrative of the Financial Crisis

1. A housing bubble inflates in the mid 2000s. Homes are financed by mortgages that are increasingly securitized. Although the quality of mortgages deteriorates, the securities into which these

mortgages are packaged are perceived to be safe and receive AAA-ratings.

2. Financial institutions such as banks and dealer banks retain substantial exposure to the real estate market through direct holdings of commercial real estate and direct holdings of mortgage-backed securities, but also through implicit guarantees of special investment vehicles they organize that hold mortgage-backed securities and finance them with commercial paper.

3. Bad news about the housing market in the summer of 2007 surprises investors in AAA-rated mortgage-backed securities and precipitates a sequence of substantial disruptions in financial markets, such as the collapse of the asset-backed commercial paper market. Aggressive liquidity interven-tions from the Federal Reserve, including lending to market participants against risky collateral, stabilize markets through the summer of 2008 despite continued bad news about housing.

4. In September 2008, several events, including a run on money market funds, nationalization of AIG, Fannie Mae, and Freddie Mac, and particularly the collapse of Lehman Brothers, precipitate

a massive financial crisis. Banks’ balance sheets contract because of massive losses on assets and withdrawal of short-term financing, which prompts banks to liquidate assets in i re sales. The con-sequences of fire sales are exacerbated by uncertainty about bank solvency and government policy.

5. In response to their losses and to reduced availability of financing, banks cut lending to firms.

6. The economy slides into a major recession.

7. Starting in October 2008, the government begins massive interventions in financial markets,

including equity injections in banks, expansion of lending against risky collateral, but also direct

purchases of long-term agency bonds, which sharply reduce the supply of risky bonds in the market. The combination of government interventions eventually stabilizes the financial markets by spring 2009, although the real economy remains sluggish.

"The Quiet Coup" by Simon Johnson

The crash has laid bare many unpleasant truths about the United States. One of the most alarming, says a former chief economist of the International Monetary Fund, is that the finance industry has effectively captured our government—a state of affairs that more typically describes emerging markets, and is at the center of many emerging-market crises. If the IMF’s staff could speak freely about the U.S., it would tell us what it tells all countries in this situation: recovery will fail unless we break the financial oligarchy that is blocking essential reform. And if we are to prevent a true depression, we’re running out of time. [Continue reading]

Keynes vs Hayek

On page 39:

Table 1: A Narrative of the Financial Crisis

1. A housing bubble inflates in the mid 2000s. Homes are financed by mortgages that are increasingly securitized. Although the quality of mortgages deteriorates, the securities into which these

mortgages are packaged are perceived to be safe and receive AAA-ratings.

2. Financial institutions such as banks and dealer banks retain substantial exposure to the real estate market through direct holdings of commercial real estate and direct holdings of mortgage-backed securities, but also through implicit guarantees of special investment vehicles they organize that hold mortgage-backed securities and finance them with commercial paper.

3. Bad news about the housing market in the summer of 2007 surprises investors in AAA-rated mortgage-backed securities and precipitates a sequence of substantial disruptions in financial markets, such as the collapse of the asset-backed commercial paper market. Aggressive liquidity interven-tions from the Federal Reserve, including lending to market participants against risky collateral, stabilize markets through the summer of 2008 despite continued bad news about housing.

4. In September 2008, several events, including a run on money market funds, nationalization of AIG, Fannie Mae, and Freddie Mac, and particularly the collapse of Lehman Brothers, precipitate

a massive financial crisis. Banks’ balance sheets contract because of massive losses on assets and withdrawal of short-term financing, which prompts banks to liquidate assets in i re sales. The con-sequences of fire sales are exacerbated by uncertainty about bank solvency and government policy.

5. In response to their losses and to reduced availability of financing, banks cut lending to firms.

6. The economy slides into a major recession.

7. Starting in October 2008, the government begins massive interventions in financial markets,

including equity injections in banks, expansion of lending against risky collateral, but also direct

purchases of long-term agency bonds, which sharply reduce the supply of risky bonds in the market. The combination of government interventions eventually stabilizes the financial markets by spring 2009, although the real economy remains sluggish.

"The Quiet Coup" by Simon Johnson

The crash has laid bare many unpleasant truths about the United States. One of the most alarming, says a former chief economist of the International Monetary Fund, is that the finance industry has effectively captured our government—a state of affairs that more typically describes emerging markets, and is at the center of many emerging-market crises. If the IMF’s staff could speak freely about the U.S., it would tell us what it tells all countries in this situation: recovery will fail unless we break the financial oligarchy that is blocking essential reform. And if we are to prevent a true depression, we’re running out of time. [Continue reading]

Keynes vs Hayek

Subscribe to:

Posts (Atom)